By Life Republic Editorial Team | Published: May 22, 2025 | Updated: June 16, 2026

Read Time: 9 min

Applying for a home loan is a significant financial decision, especially for first time buyers. This comprehensive guide will help you understand the key steps involved in securing a home loan and ensure you are well-prepared for the process.

In this article, we will share essential tips for first time buyers, offering practical advice to help you navigate the home loan process with confidence.

Before you apply for a home loan, it is crucial to assess your current financial situation. Make sure you understand all your financial obligations, such as existing debts and regular payments, as these can impact your loan eligibility. Additionally, be aware of the long-term commitment to repay the entire loan amount over the loan tenure, so you are fully prepared for the responsibilities involved.

A home loan is one of the most significant financial commitments you’ll make on your journey to owning your dream home. Home loans are designed to help individuals purchase, construct, or improve residential properties, with options such as home purchase loans, home improvement loans, and construction loans available to suit different needs. Understanding the various types of home loans and how home loan interest rates, loan tenure, and eligibility criteria work is essential for making informed decisions.

When considering a home loan, it’s important to evaluate your home loan eligibility, which is determined by factors like your income, credit score, debt-to-income ratio, and employment history. A good credit score plays a significant role in both loan approval and the interest rates you’re offered. Lenders use these criteria to assess your repayment capacity and determine the maximum loan amount you can borrow. To get a clearer picture of your eligibility and the maximum loan you can avail, you can use a home loan eligibility calculator. By understanding these fundamentals, you’ll be better equipped to choose the right type of loan and secure the best possible terms for your financial situation.

Applying for a home loan is a major financial decision. Whether you’re a first-time homebuyer or an experienced investor, understanding the nuances—from home loan interest rates to your credit score—is crucial. Lenders also closely evaluate your employment history, and job stability is a key factor in their assessment of your repayment capacity and financial reliability. When reviewing your debt-to-income ratio, managing existing debts—such as repaying smaller loans or consolidating what you owe—can improve your eligibility for a home loan. Additionally, be sure to consider other financial obligations, like student loans or car payments, that may impact your ability to afford a home loan. Let’s break it down so you can confidently secure the best deal.

Meeting the eligibility criteria is a crucial first step in securing a home loan. While requirements may vary among financial institutions, most lenders focus on several key factors. Your income, age, credit score, and employment history are all carefully evaluated to determine your loan eligibility. Lenders will review your credit report and assess your debt-to-income ratio to ensure you have the repayment capacity to handle the home loan EMI over the chosen loan tenure.

A stable employment history and a good credit score can significantly improve your chances of loan approval and help you secure a more favorable interest rate. The loan amount you qualify for will also depend on these factors, as well as the interest rate and repayment terms offered by the lender. To plan your finances and estimate your monthly payments, you can use a home loan EMI calculator. By understanding and meeting the eligibility criteria, you’ll be in a stronger position to negotiate your loan terms and move forward confidently in the home loan process.

Before diving into the market, it’s important to know what type of loan suits you:

1. Fixed-Rate Home Loans: Interest rates remain constant throughout the loan tenure.

2. Floating Rate Loans: These loans have variable interest rates that may change based on market benchmarks, offering flexibility as rates fluctuate with market conditions.

3. Home Loan Balance Transfer: Transfer an existing loan to a new lender offering better rates.

4. Government Subsidy Loans: Special schemes like PMAY (Pradhan Mantri Awas Yojana) offer reduced rates.

Pro Tip: Always compare the current home loan interest rates before finalizing.

Explore different loan options to find the best fit for your financial situation.

Your credit score is a crucial factor that lenders assess.

1. Check Your Score Regularly: Use platforms like CIBIL, Experian.

2. Reduce Credit Card Dues: Maintain a low credit utilization ratio.

3. Avoid Frequent Loan Applications: Too many inquiries can lower your score.

4. Clear Old Debts: Even a single default can impact your eligibility.

Lenders may also review pay stubs, along with other documents, to assess your financial profile during the home loan application process.

Did you know? A score above 750 significantly boosts your chances of getting a lower home loan interest rate in India.

Borrow smartly, not excessively.

1. EMI Rule: Ideally, your EMI should not exceed 30%-40% of your monthly income. Each EMI consists of both interest and principal repayment, so understanding this breakdown is important for long-term planning.

2. Down Payment Planning: Aim for at least 20% down payment.

3. Consider Hidden Charges: Processing fees, legal fees, GST, and insurance premiums add up.

4. Emergency Fund: Always maintain reserves for 6-9 months of EMI payments.

5. Factor in Property Taxes: Remember to include property taxes as a recurring expense when calculating affordability.

When planning your loan, choose an appropriate repayment tenure to balance monthly affordability and the total interest paid over the life of the loan.

Use a Home Loan EMI calculator online to budget efficiently.

The home loan application process involves several important steps designed to assess your financial position and ensure you meet the lender’s requirements. To begin, you’ll need to gather and submit essential documents, such as ID proof, income tax returns, and recent bank statements. Most financial institutions will also require a credit check as part of the loan application process.

You can apply for a home loan either online or by visiting a bank branch, and the processing time may vary depending on the lender and the complexity of your application. Including a co-applicant can sometimes help you qualify for a higher loan amount. During the application process, you’ll have the opportunity to negotiate the interest rate and other loan terms with your lender. Before signing, it’s vital to carefully read and understand the loan agreement, as it outlines all the terms and conditions of your home loan. For more information on the application process or to clarify any doubts, you can contact the lender’s toll-free number or visit their official website.

To ensure a smooth home loan application process, it’s important to have all the required documents ready and up-to-date. Typically, you’ll need to provide ID proof, address proof, income tax returns, salary slips, and recent bank statements. If you’re self-employed, additional documents such as business proof and financial statements may be necessary. Property documents, including the title deed and sale agreement, are also required to verify the legitimacy of the property you intend to purchase.

A good credit score and a stable employment history can further strengthen your application and improve your chances of loan approval. Using a home loan eligibility calculator can help you determine your loan eligibility and identify the documents you’ll need to submit. Ensuring all paperwork is complete and accurate will help avoid delays and make the home loan process as efficient as possible.

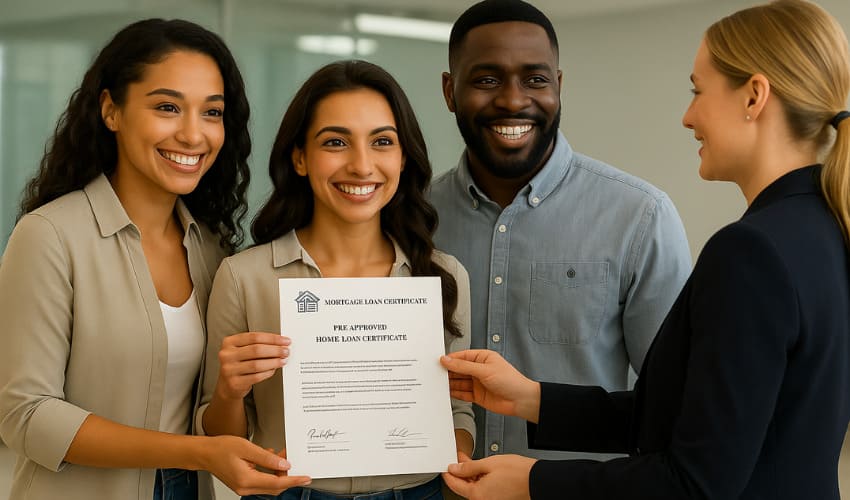

1. Pre-Qualification: A rough estimate of the loan amount you might qualify for, based on basic financial inputs.

2. Pre-Approval: A more detailed process involving credit checks and documentation review by the lender. Pre-approval helps you understand your borrowing capacity and strengthens your position when making an offer. The pre-approval involves a detailed approval process, including submitting documentation and a thorough financial review to determine your eligibility and loan terms.

Tip: Pre-approval strengthens your negotiating power with sellers and gives you an edge in competitive markets, as it signals to sellers that you are a serious buyer.

Not all lenders are the same.

1. Compare Offers: Use online marketplaces or consult multiple banks. Prioritize lenders that offer competitive interest rates to ensure affordability and maximize your savings.

2. Check Flexibility: Look for flexible repayment options or part-payment facilities.

3. Current Trends: As of 2025, current home loan interest rates in India vary between 8.25% - 9.15% depending on the borrower profile.

Always check floating vs. fixed interest options based on your future financial plans.

Applying for a home loan involves more than just choosing a lender—it requires thorough planning, understanding your financial profile, and making informed comparisons. From improving your credit score to choosing between fixed or floating interest rates, every step plays a vital role in securing the best deal. As you prepare to invest in your dream home, don’t forget to explore pre launch projects in Hinjewadi Pune, which often come with attractive pricing and flexible payment plans. Whether you’re looking for investment opportunities or planning to move in, flats in Hinjewadi offer a great combination of modern living and long-term value. When selecting a property, consider options with good resale value to enhance your investment potential and future flexibility.

Q1: What is a good credit score to apply for a home loan?

A1: A score above 750 is considered excellent and increases your chances of lower interest rates.

Q2: How do I find the current home loan interest rates?

A2: You can check on bank websites, loan aggregator portals, or consult directly with banks and NBFCs.

Q3: Should I go for a fixed or floating home loan interest rate?

A3: Fixed rates offer stability, while floating rates may save you money if the market trend is downward.

2 and 3 BHK Flats at Qrious, Life Republic Hinjewadi

Possession: April 2030

RERA: Rera No - P52100079623

Starting price from Rs. 85 Lakhs*

Copyright 2026 Life Republic. All Rights Reserved.

Sitemap | Privacy Policy | Terms and Conditions | Cookie Policy

Life Republic R16 (16th Avenue) | Sound of Soul: P52100048241 as Life Republic R17 A | Nora: P52100022278 Life Republic Sector R17 - B 17 B Avenue - Nora. | Atmos Phase I- P52100051765 as Life Republic/Sector R22/22nd Avenue/Atmos/Phase - Available at website: http//maharera.mahaonline.gov.in under registered projects. *T & C Apply.